Info Centre

Property Info CentreSome useful information here at our Property Info Centre, and HOT TOPICS to help you with your property transactions.

CONTENT (you may jump to any of the section by clicking on the content below:

Ever wonder how to SELL ONE, BUY TWO PROPERTIES?

Let us help you using our in-house professional restructuring tool

- Loan Calculator

- Progressive Payment Calculator

- Sales Proceeds Calculator

- Mortgage or Refinance Calculator

- TSDR and ABSD Calculator

- Should you do decoupling? What is decoupling?

- 99/1 strategy. What is 99/1 strategy?

Calculators

New Launch vs Resale Properties

New Launch vs Resale?

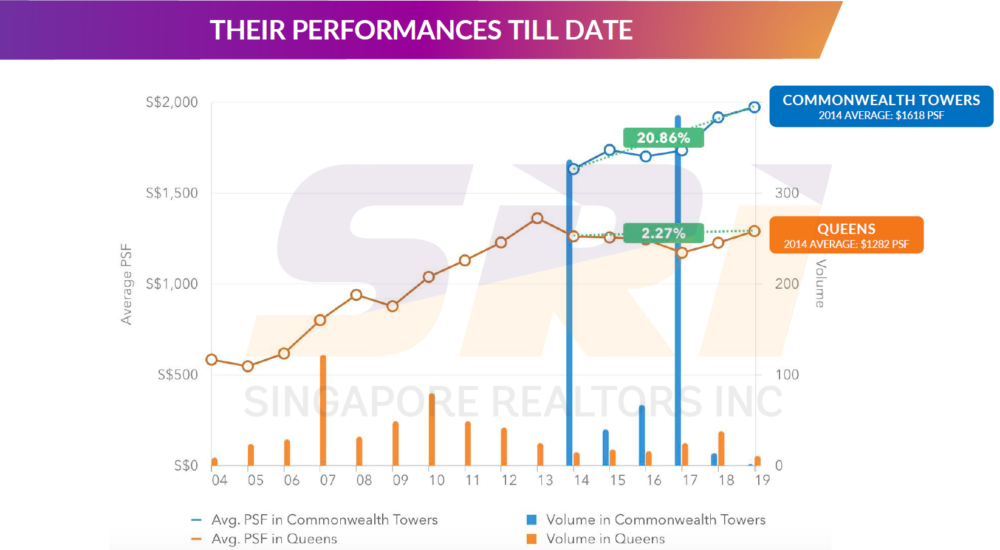

A typical chart comparing between New Launch and Resale

The above chart is what you would usually see if you are comparing between buying a New Launch and Resale residential unit. Hence, how to decide between the 2 will depends on what matters to you more. Would you prefer to buy a new home with newer facilities? Want more flexibility in your down payment and monthly mortgage? To achieve capital appreciation? Then a new launch condo is for you.

On the other hand, if you want to move in or rent out for immediate rental income, then a resale condo is a no-brainer. If you know where to head for your house hunting, you can look for good bargains in the market, and might get your hands on an undervalued property.

While property generally appreciate in value, other factors do have an impact on the value. So, do remember that factors such as location, nearby amenities, remaining lease, and now proximity to good SCHOOLS will contribute to the value of the property.

Moreover, MOE has recently released an update on Phase 2C vacancy. As a result, more home buyers are buying their homes near good schools. This has been the trend in recent years because it is very important for parents to cut down travelling time when they send their children to school. Therefore, it is definitely an ideal choice to buy a property near good schools. This is one of the factor to push up property prices in these area.

Buying a condo can be a good investment, but always work out your finances accordingly. You should also consider other factors such as the amount of bank loan you can borrow, the location, and upcoming government transformation plans. These will thus help you to decide what, which, where and when to buy.

Leasehold vs Freehold Properties

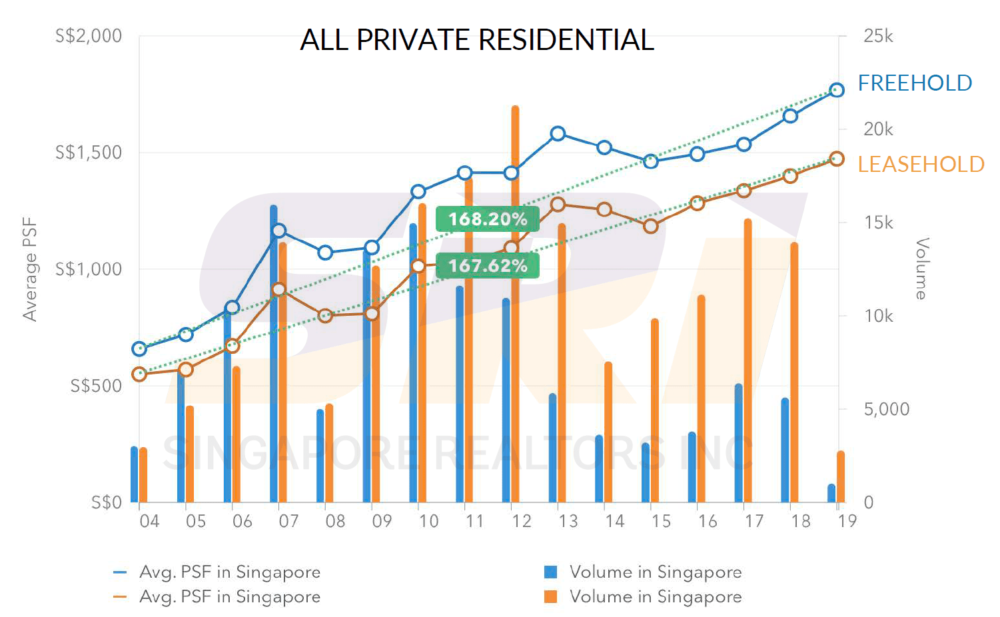

Leasehold vs Freehold?Property ownership in land-scare Singapore largely consists of freehold and leasehold estates. Of late, most of the new launches come with 99-year leasehold tenur. Especially so for those that are within short distance to a MRT Station.

A freehold property can be held by the owner indefinitely. While, a leasehold property reverts back to the state upon the expiry of its lease.

At first glance, it may seem that freehold property is much more attractive than the leasehold property. But wait a minutes! This may not be necessarily true.

There are provisions that allow the government to reclaim the land for vital infrastructure or security purposes. If your house is in the way of a major highway, the fact that it’s freehold is not going to save it. Besides, there is also the possibility of enbloc redevelopment. If a developer makes an enbloc attempt for your freehold condo, and the majority of the residents agree to it, then you’re still going to be moving out.

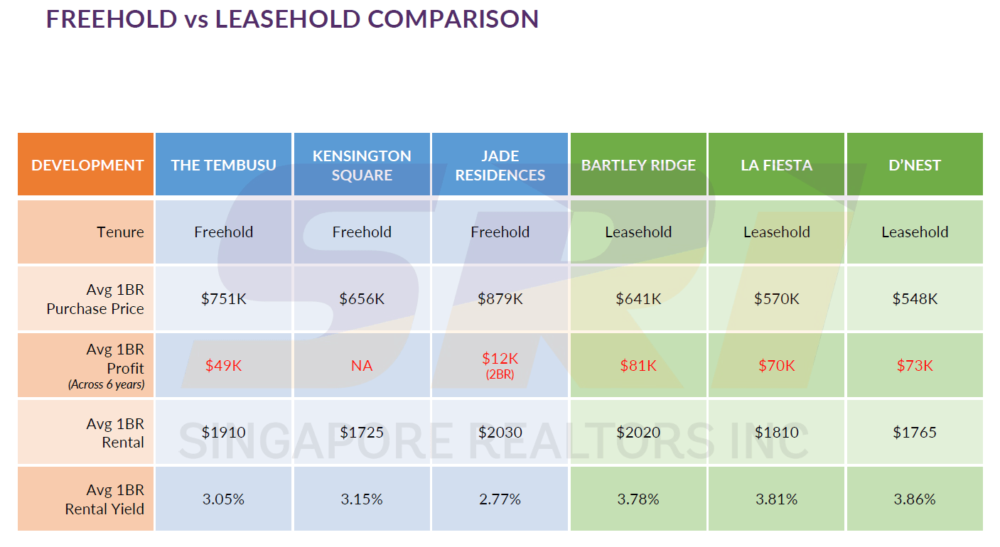

Quite the norm, the initial sale price of a freehold unit (new sale) tends to be 15 to 20 percent higher, or even more than 20% higher, as compared to a leasehold unit in the same area. If you are buying a unit for investment, to rent out, tenant will be indifferent to the tenure of the property.

Therefore, if you are a property owner looking to buy a property for rental income, you should consider the 99-year leasehold development. Of course this will also depends on your longer term plan. This is because leasehold is better for rental yield since your initial capital is lower. As higher property purchase price will eats into the rental yield which you can earn from your rental investment. Take a look at the table below for some examples.

The value of a property is determined by many factors other than tenure of the land itself.

While freehold properties are indeed more scarce, it does not always result in a better price. Buyers looking for a home are likely to care more about the location and amenities around the property rather than whether they can hold onto the property for long.

One of the trending criteria recently when a buyer select a property is the distance to reputable schools. This is true for both the local and foreign buyers.

Sending kids to school is an everyday task. And parents can save on travelling time if the kids are enrolled in a school nearby. We are seeing more home buyers buying their homes near reputable schools, as mentioned earlier on this page. Thus, this will be a factor to push up demand and property prices in such locations.

However, freehold private properties outperformed their leasehold counterparts for the older developments (around 21 - 30 years old). This is especially so for those owners who bought during the initial launch of the development. The value appreciation for freehold properties are not as affected by the age of the property. In contrast, leasehold properties will see more significant capital appreciation in the earlier stages of the tenure, while seeing a decline in capital appreciation rate as they are nearing the end of the lease tenure.

Thus, it will be more practical for home buyers or investors who are interested in capital appreciation to consider factors such as location and accessibility. Factors such as amenities within the neighborhood as well as upcoming developments around the vicinity are also important.

Singapore Property Rules & Policies

Rules & Policies

- Rules for New Housing Loans

- Buyer Stamp Duty (BSD) & Additional Buyer Stamp Duty (ABSD)

- Seller Stamp Duty (SSD)

- Executive Condominium (EC) Eligibility

- CPF Housing Grant for EC

- CPF Minimum Sum

Rules for New Housing Loans

Below is a chart Loan-To-Value Summary.

The maximum housing loan borrowers can take depends on their age, loan duration and property type, as well as whether they have other existing housing loans. While joint borrowers are assessed using an income-weighted average age.

The maximum loan tenure for housing is capped at 30years for HDB flats and 35years for non-HDB properties, up to the age of 65 years old.

The current Loan-to-Value (LTV) limit is 75% from financial institutions. For buyers buying a HDB flat and taking a loan from HDB, the current Loan-to-Value is 80%. Check with us if you would like to have an estimate of your loan quantum.

MSR Rules

Mortgage servicing ratio (MSR) refers to the portion of a borrower’s gross monthly household income that goes towards repaying all property loans, including the loan being applied for.

MSR is capped at 30% of a borrower's gross monthly household income. And this applies only to housing loans for the purchase of a BTO flat from HDB or an executive condominium from a developer.

Calculating MSR

When calculating MSR, Financial Institutions take into consideration the following:

- All the borrower’s property loans, and

- At least 20% of the monthly debt obligation for any property loan where the borrower is a guarantor.

To calculate a borrower’s MSR, use the following formula:

(Monthly repayment instalments for all property loans / Gross monthly Income) x 100% ≤ 30%)

TDSR Rules

Total debt servicing ratio (TDSR) refers to the portion of a borrower’s gross monthly income that goes towards repaying the monthly debt obligations, including the loan being applied for.

With the recent cooling measures in December 2021, a borrower's TDSR should be less than or equal to 55%.

Still unsure about how the loan mechanism works? We can assist you! We can arrange for a mortgage officer to speak with you.

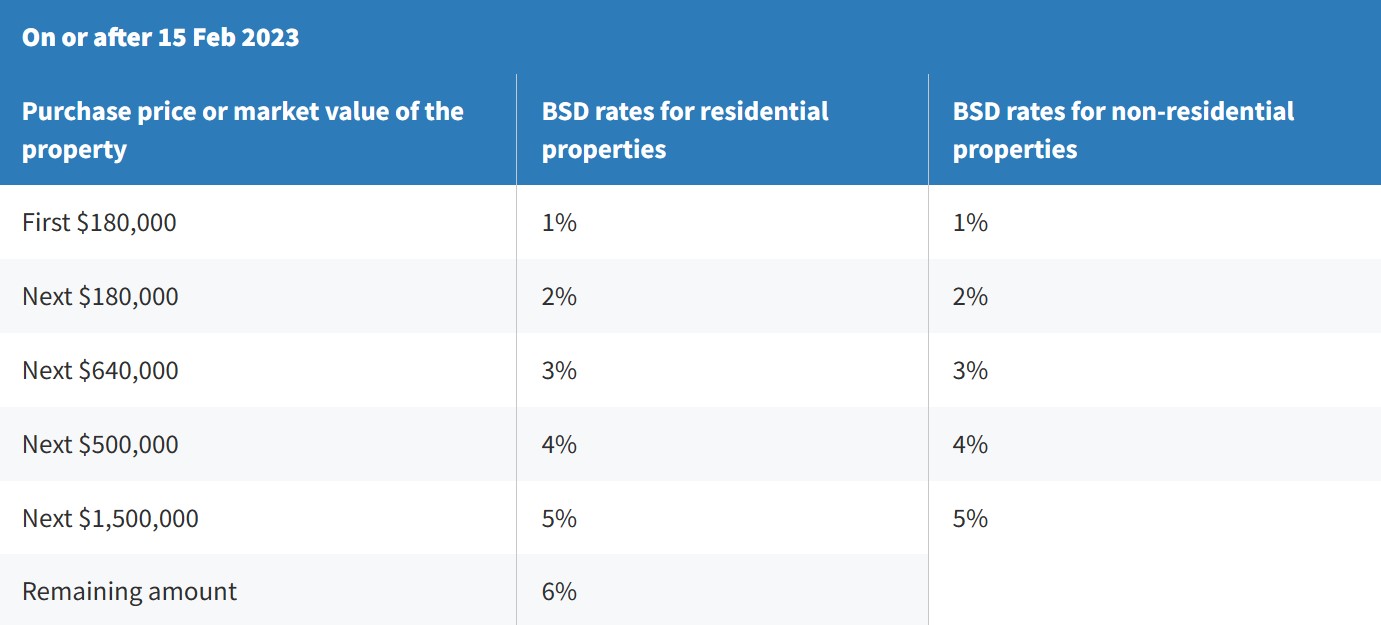

Buyer Stamp Duty (BSD)/Additional Buyer Stamp Duty (ABSD)

Below is a table showing rates based on residency status.

With effect from 15th February 2023, BSD rates of up to 5% is applicable to purchase of non-residential properties. While BSD rates of up to 6% is chargeable for purchase of residential property.

ABSD of up to 30% (for foreigners) may also be applicable. ABSD rates have been revised, up to 35% (for foreigners) with the latest cooling measures effective 16 December 2021. Take a look at the table above for the different tiers of ABSD.

Liable buyers are required to pay ABSD on top of the existing Buyer’s Stamp Duty (BSD). ABSD and BSD are computed on the purchase price as stated in the dutiable document or the market value of the property (whichever is the higher amount).

The ABSD liability will depend on the profile of the buyer as at the date of purchase of the residential property:

A. Whether the buyer is an individual or an entity

B. The residency status of the buyer and

C. The count of residential properties owned by the buyer

Latest change in purchase under trust deed also see a 35% ABSD chargeable. Buyers buying under trust can apply for ABSD refund when specific terms and conditions are met. Check with us for more info!

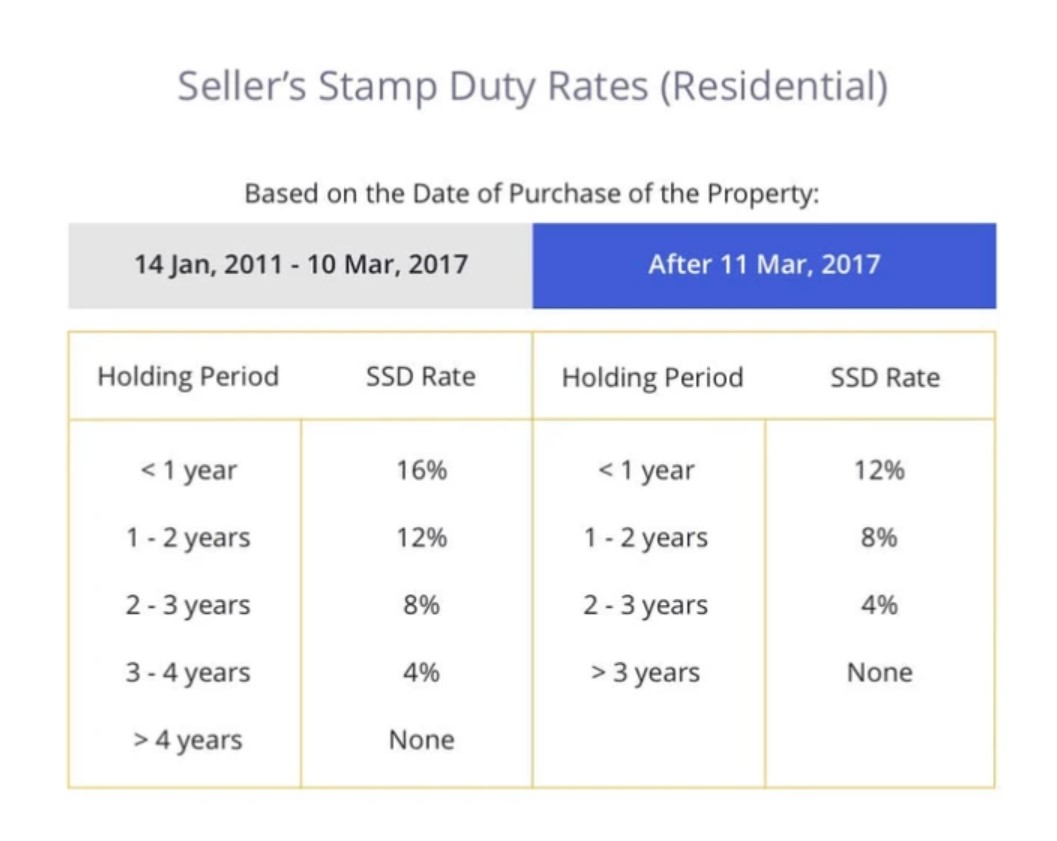

Seller Stamp Duty (SSD)

Here's what you need to pay if you sell your Private Residential Property within 3 year of purchase.

SSD is payable for residential and industrial properties acquired on or after 20 Feb 2010, if the property is disposed off within the holding period.

In most instances, the date of purchase/acquisition of a property refers to:

- Date of Acceptance of the Option to Purchase* or

- Date of Sale and Purchase Agreement or

- Date of Agreement for Lease (for new HDB flat) or

- Date of Transfer where the above (a), (b) and (c) are not applicable

* Excludes an Option to Purchase that is subject to the execution/signing of the Sale and Purchase Agreement.

**SSD table above shows rates payable for disposing off residential properties within the holding period.

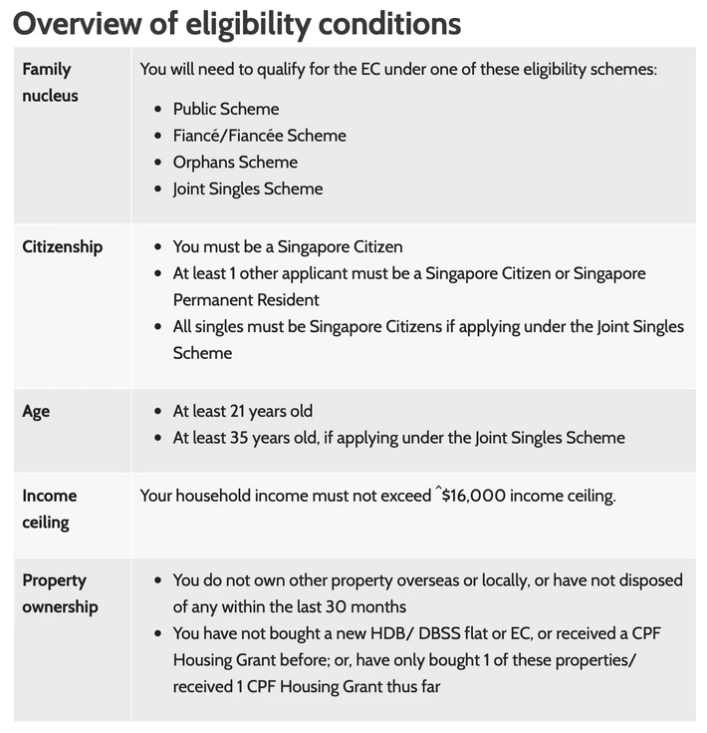

Executive Condominium (EC) Eligibility

ECs are comparable to private condo in terms of design and facilities. But Private developers are the ones who build and sell them instead of HDB. And they are attractive options for higher-income Singaporeans. Since ECs are governed by HDB, they are thus subject to the eligibility conditions as per those applying for a Built-to-Order (BTO) Flats. Except, the average gross monthly household income must not exceed $16,000 instead of $14,000.

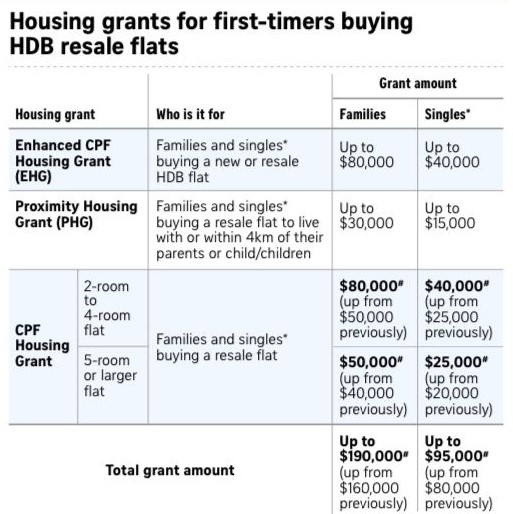

CPF Housing Grants for EC

Based on gross monthly household income

The income ceiling to apply for CPF Housing Grant is an average gross monthly household income of not more than $12,000. You are considered a first-time applicant if you have not received any housing subsidy from HDB. Therefore you must not:

- Be the owner of a flat bought from HDB.

- Have sold a flat bought directly from HDB.

- Have taken the CPF Housing Grant to buy an EC; Design, Build and Sell Scheme (DBSS) flat; or an HDB resale flat; or taken over ownership of such a flat or EC.

- Have transferred the ownership of a flat bought directly from HDB, or an HDB resale flat bought with a CPF Housing Grant.

- Have ever taken other forms of housing subsidy, such as Selective Enbloc Redevelopment Scheme (SERS) benefits or privatisation of HUDC estate.

You can apply for the Citizen Top-Up when a qualifying member of your SC/ SPR household obtains Singapore citizenship. And you need to submit your application to HDB within 6 months of being eligible for it.

CPF Housing Grants are fully credited into the CPF Ordinary Accounts of eligible Singapore Citizen (SC) applicants. Hence, no cash is disbursed.

Application for EC CPF Housing Grant is submitted to the developer during booking of the EC unit.

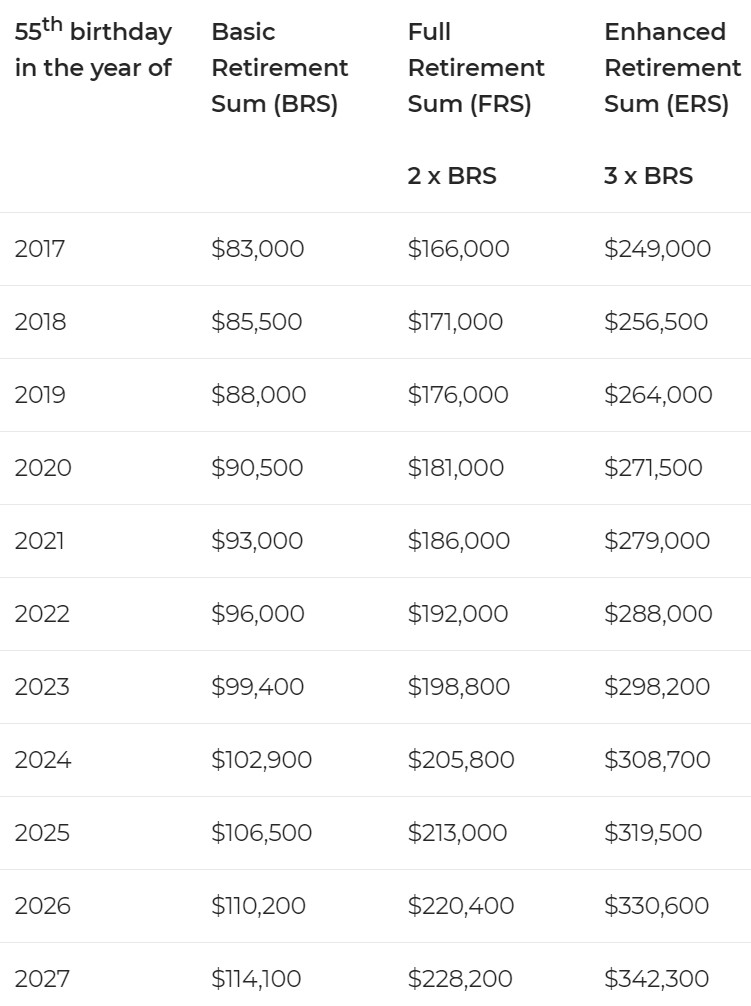

What is CPF minimum Sum?

A table showing the FRS and BRS

*Source from CPF Board

The Minimum Sum (Full Retirement Sum) is the amount that must be set aside in the Central Provident Fund (CPF) for retirement needs when a member turns 55. Half (Basic Retirement Sum) can be in the form of a pledge from a property purchased with CPF savings. This Minimum Sum provides CPF members with monthly payouts in their retirement years.

If you are intending to purchase a 2nd property, and have already used CPF for your 1st property, you can only use the excess CPF Ordinary Account savings after setting aside the current Basic Retirement Sum.

Singapore Resale Properties & New Launches

Pros & Cons of DIY

Why are there many people who do not DIY their own property transactions?

Transaction processes have been streamlined to allow DIY. But most home buyers and sellers are still engaging real estate agents to represent them in the buying, selling and leasing of their properties. Why is this so?

They may not possess complete set of knowledge for a smooth and thus, a successful transaction. Although, transaction process may not be complicated, it is neither simple. Therefore, a simple mistake can be very costly and stressful. Most of the information on pricing, market condition, trends and regulations are becoming more readily available on the internet. But, it takes years of practice and experience to get some analysis from the mountain of data, and they may not be as straight-forward as they seem to be.

Property transaction is not just about the process itself. Psychology and emotions of sellers and buyers, staging of the properties we are marketing to make them look more appealing, handling objections of prospective buyers, etc are some basic skill sets that are required, as well as time consuming. As professional real estate agents, we are able to offer different opinions and point of views as a neutral party.

Time Consuming

If you are selling your property, can you imagine yourself dealing with continuous enquiries coming in any time in the day and night? Even past midnight? And handling same enquiries over and over again? Or dealing with DIY buyers, who learn to DIY from reading online yet who may not know everything about a transaction? While handle hectic and tiring viewing appointments? Buyers late for appointments? Unpleasant feedbacks and low ballers? No-show? These are some of the things you will need to handle. Unknowing to many, real estate agents have helped to shield these from their sellers. With us as an intermediary, we are able to stay neutral. This will therefore help in negotiation, allow you to make more rational decision and to achieve a win-win situation. Your time is precious. Hence, leave all these time-consuming chores, entertaining many viewing appointments and leg work to us.

The above are some basic rules and policies at our Property Info Centre for your reference. Feel free to contact us to understand more.